How to Finance Hawaii Condo: Step-by-Step Oahu Guide

Did you know that the average price of a condo in Oahu tops $500,000? Buying a home in paradise means more than just sunny beaches. How to finance hawaii condo It demands smart financial planning and careful loan selection to avoid costly surprises. Whether you are a first-timer or upgrading, understanding Hawaii condo financing can help you secure a place that truly fits your budget and long-term dreams.

Table of Contents: How to Finance Hawaii Condo

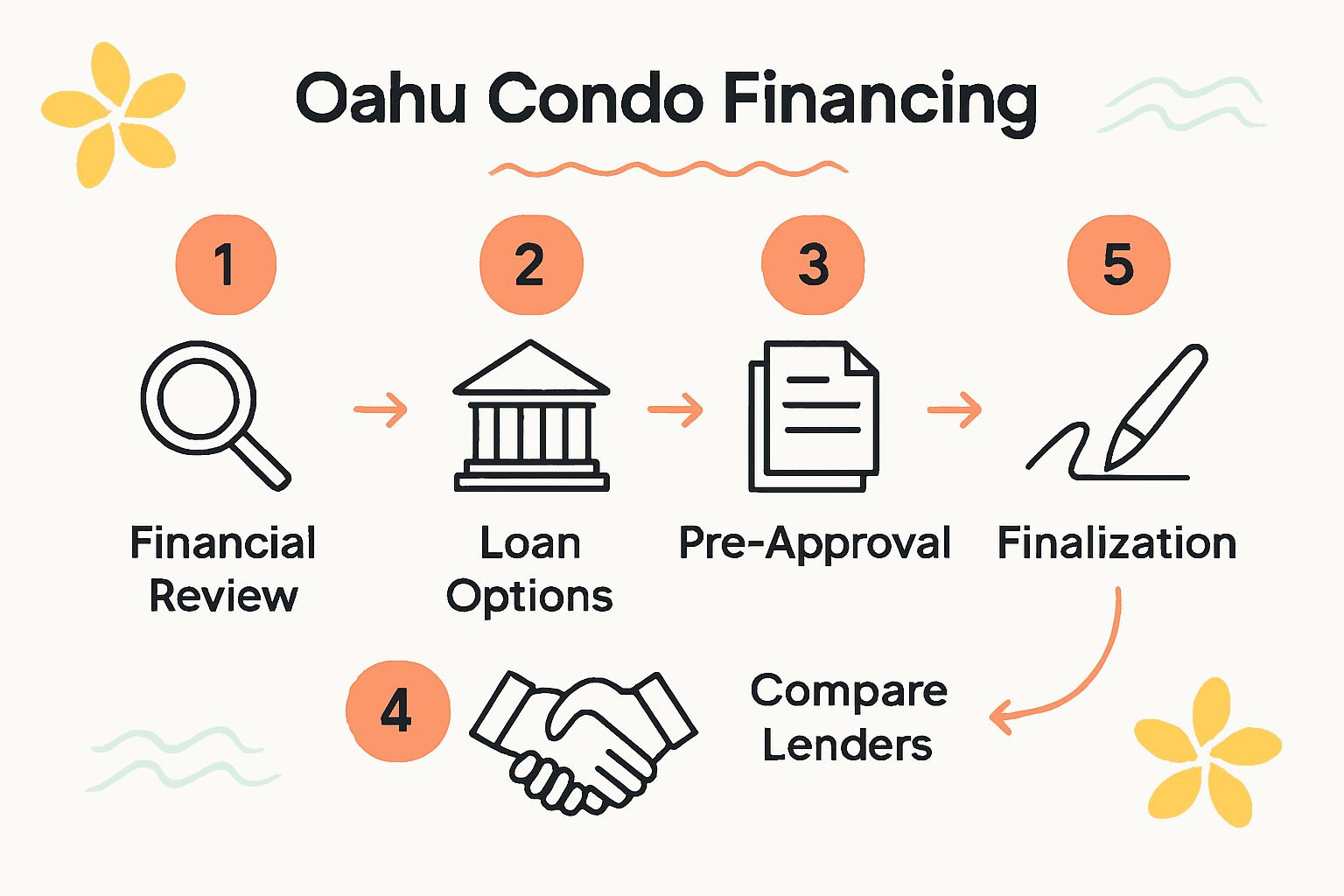

- Step 1: Assess Your Financial Readiness

- Step 2: Explore Hawaii Condo Loan Options

- Step 3: Get Pre-Approved For Financing

- Step 4: Select Suitable Lenders And Compare Rates

- Step 5: Finalize And Verify Your Hawaii Condo Loan

Quick Summary

| Key Point | Explanation |

|---|---|

| 1. Assess Financial Readiness | Evaluate your credit score, debts, and savings to determine if you’re ready to buy a condo. |

| 2. Explore Loan Options | Research various financing options like conventional, FHA, and USDA loans that best fit your situation. |

| 3. Get Pre-Approved | Gather necessary documents and obtain pre-approval to know your budget and strengthen your position as a buyer. |

| 4. Compare Lenders | Investigate different lenders and their offers, focusing on rates, fees, and customer service for the best deal. |

| 5. Finalize Loan Details | Review and confirm loan terms to ensure they match your expectations before signing any documents. |

Step 1: Assess Your Financial Readiness

Let’s dive into understanding your financial landscape for purchasing a Hawaii condo. This crucial first step involves thoroughly evaluating your current financial health and determining whether you’re ready to make a significant real estate investment in Oahu.

Start by pulling together a comprehensive financial snapshot. Review your credit score, total monthly income, existing debts, and savings. Most lenders prefer credit scores above 620 for condo financing, with 700 or higher securing the best interest rates. Calculate your debt to income ratio by dividing your monthly debt payments by your gross monthly income. Ideally, you want this ratio under 43% to demonstrate financial stability.

According to the Hawaii Foreclosure Information Center, understanding loan terms and recognizing potential financial risks is critical when pursuing property financing. Be prepared to provide documentation like tax returns, pay stubs, bank statements, and employment verification. Pro tip: Get pre approved before serious house hunting. This not only clarifies your budget but also shows sellers you’re a serious buyer.

Check your emergency savings too. Aim to have at least 3-6 months of living expenses set aside beyond your down payment. This financial cushion protects you from unexpected costs and demonstrates financial responsibility to potential lenders. Your next step? Schedule a meeting with a local mortgage professional who understands Oahu’s unique real estate market.

Step 2: Explore Hawaii Condo Loan Options

Now that you’ve assessed your financial readiness, it is time to explore the diverse loan options available for purchasing a condo in Oahu. Your goal in this step is to understand the different financing paths and identify which loan type best matches your financial profile and real estate objectives.

Multiple loan options exist for potential condo buyers. Conventional loans through banks typically require 10-20% down payments and offer competitive interest rates for borrowers with strong credit. FHA loans provide more flexible qualifying standards, allowing lower credit scores and down payments as low as 3.5%. According to Hawaii Central Federal Credit Union, Home Equity Lines of Credit can also be an attractive option for those with existing property equity, offering introductory rates and flexible borrowing terms.

Alternative financing routes are worth exploring too. USDA Direct Home Loans present another financing avenue, particularly for first time buyers or those in specific income brackets. They offer fixed interest rates and extended repayment periods.

Pro tip: Get quotes from multiple lenders and compare not just interest rates, but also closing costs, loan terms, and potential prepayment penalties. Your next step? Schedule consultations with mortgage professionals who specialize in Oahu condo financing to get personalized recommendations tailored to your specific financial situation.

Pro tip: Get quotes from multiple lenders and compare not just interest rates, but also closing costs, loan terms, and potential prepayment penalties. Your next step? Schedule consultations with mortgage professionals who specialize in Oahu condo financing to get personalized recommendations tailored to your specific financial situation.

Step 3: Get Pre-Approved for Financing

Getting pre-approved for a condo loan is a critical milestone in your Oahu real estate journey. This process transforms your home buying dreams from wishful thinking into a concrete financial strategy, giving you a clear understanding of exactly how much you can borrow and demonstrating to sellers that you are a serious buyer.

To begin the pre-approval process, gather all necessary financial documentation. According to the Hawaii Housing Finance and Development Corporation, you will need to prepare comprehensive paperwork including recent tax returns, pay stubs, bank statements, employment verification, and detailed information about your assets and debts. Most lenders will conduct a thorough review of your credit history, examining your credit score, income stability, and debt to income ratio.

Hawaii Central Federal Credit Union recommends obtaining pre-approval from multiple lenders to compare rates and terms. Pro tip: Get pre-approved within a 14 day window to minimize impact on your credit score, as multiple inquiries during this period are typically counted as a single credit pull. The pre-approval letter you receive will specify the maximum loan amount you qualify for, interest rate, and potential loan terms. Your next step? Use this pre-approval as a powerful negotiation tool when you start touring Oahu condos and making offers.

Step 4: Select Suitable Lenders and Compare Rates

Selecting the right lender is a pivotal moment in your Oahu condo financing journey. Your goal is to find a lending partner who offers competitive rates, understands the unique Hawaii real estate market, and provides personalized support tailored to your specific financial needs.

Start by exploring multiple lending institutions with experience in Oahu condo financing. According to Hawaii Central Federal Credit Union, local credit unions often provide more flexible and competitive loan products compared to traditional banks. Research lenders who specialize in condo financing and have deep understanding of Hawaii’s real estate landscape. Key factors to compare include interest rates, loan origination fees, down payment requirements, and potential prepayment penalties.

Beyond comparing numerical rates, evaluate each lender’s reputation and customer service. Maui County Federal Credit Union recommends requesting detailed loan estimates from at least three different lenders to ensure comprehensive comparison. Pro tip: Pay attention to the annual percentage rate (APR), which includes both interest rate and additional loan fees. This provides a more accurate picture of total borrowing costs. Your next step? Schedule consultations with these lenders to discuss your specific financing needs and get personalized rate quotes for your Oahu condo purchase.

Step 5: Finalize and Verify Your Hawaii Condo Loan

Congratulations on reaching the final stage of your condo financing journey. This critical phase involves carefully reviewing and confirming all loan details to ensure you fully understand the terms and conditions of your mortgage for your Oahu condo purchase.

According to Hawaii Central Federal Credit Union, the loan finalization process requires meticulous documentation verification. Carefully review your loan estimate and closing disclosure documents, checking for accuracy in loan amount, interest rate, monthly payments, and closing costs. Pay special attention to any adjustable rate components, prepayment penalties, and additional fees that might impact your long term financial planning.

Maui County Federal Credit Union recommends conducting a final comprehensive review before signing any documents. Pro tip: Request a final walk through of all loan terms with your lender, asking detailed questions about any clauses or conditions you do not fully comprehend. Verify that the loan terms match your initial pre approval and align with your financial goals. Your next step? Schedule a closing meeting to sign final documents and officially secure your Oahu condo financing.

Bring all required identification and be prepared to complete the last steps of your real estate investment journey.

Bring all required identification and be prepared to complete the last steps of your real estate investment journey.

Secure Your Dream Hawaii Condo with Confidence

Navigating the financial steps to purchase a condo in Oahu can feel overwhelming. From assessing your financial readiness, exploring loan options, to getting pre-approved and selecting the right lender, every stage demands careful attention and clarity. You want to avoid surprises, minimize stress, and secure the best deal possible for your dream property.

BuyOahuCondos.com is here to guide you through this complex journey. Our resource-rich platform offers practical insights and actionable advice, especially within our Oahu Condo Buying Tips | Honolulu & Waikiki Advice category, helping you master key financing concepts like pre-approval, loan comparisons, and closing details.

Take control of your condo purchase today. Explore expert tips, market updates, and personalized property listings at BuyOahuCondos.com. Start with our Oahu Condo Market Updates | Honolulu & Waikiki Reports to stay informed on current trends. Don’t wait to make your vision a reality—empower yourself with knowledge and trusted support now.

Frequently Asked Questions

How do I assess my financial readiness to finance a Hawaii condo?

To assess your financial readiness, review your credit score, monthly income, existing debts, and savings. Calculate your debt-to-income ratio, aiming for it to be below 43%, and ensure you have 3-6 months of living expenses saved for emergencies.

What loan options are available for financing a Hawaii condo?

There are several loan options available, including conventional loans, FHA loans, and Home Equity Lines of Credit. Explore these options to find which one suits your financial profile, such as looking for lower down payment requirements with FHA loans or competitive rates with conventional loans.

How do I get pre-approved for a condo loan in Hawaii?

To get pre-approved, gather necessary financial documents like tax returns and bank statements. Submit them to a lender, who will evaluate your credit and offer a pre-approval letter indicating the maximum loan amount you qualify for and interest rates.

What should I compare when selecting a lender for my Hawaii condo financing?

When selecting a lender, compare interest rates, loan origination fees, down payment requirements, and customer service reputation. Request loan estimates from at least three lenders to see who offers the best overall terms and APR.

How can I verify the details of my Hawaii condo loan before finalizing?

Carefully review your loan estimate and closing disclosure documents for accuracy on loan amounts and fees. Schedule a final discussion with your lender to clarify any terms you do not understand and ensure they align with your financial goals.

What steps should I take during the finalization of my condo loan?

During finalization, conduct a thorough examination of your loan documents, emphasizing accuracy in terms and conditions. Prepare for your closing meeting by collecting required identifications and confirming all details align with your previous agreements.

10 Comments