50‑Year Mortgage: Everything You Need to Know

More Americans are searching for creative ways to manage housing costs, and 50-year mortgages are emerging as a rare but intriguing option. With home prices reaching new highs, many people find traditional loan terms out of reach. Understanding the structure and long-term impact of a 50-year mortgage can help buyers decide if this extended repayment plan truly eases monthly budgets or creates bigger financial risks down the road.

Table of Contents

- What Is a 50‑Year Mortgage?

- How 50‑Year Mortgages Work

- Calculated Pros for Buyers

- Major Drawbacks and Financial Risks

- Alternatives to 50‑Year Mortgages

Key Takeaways

| Point | Details |

|---|---|

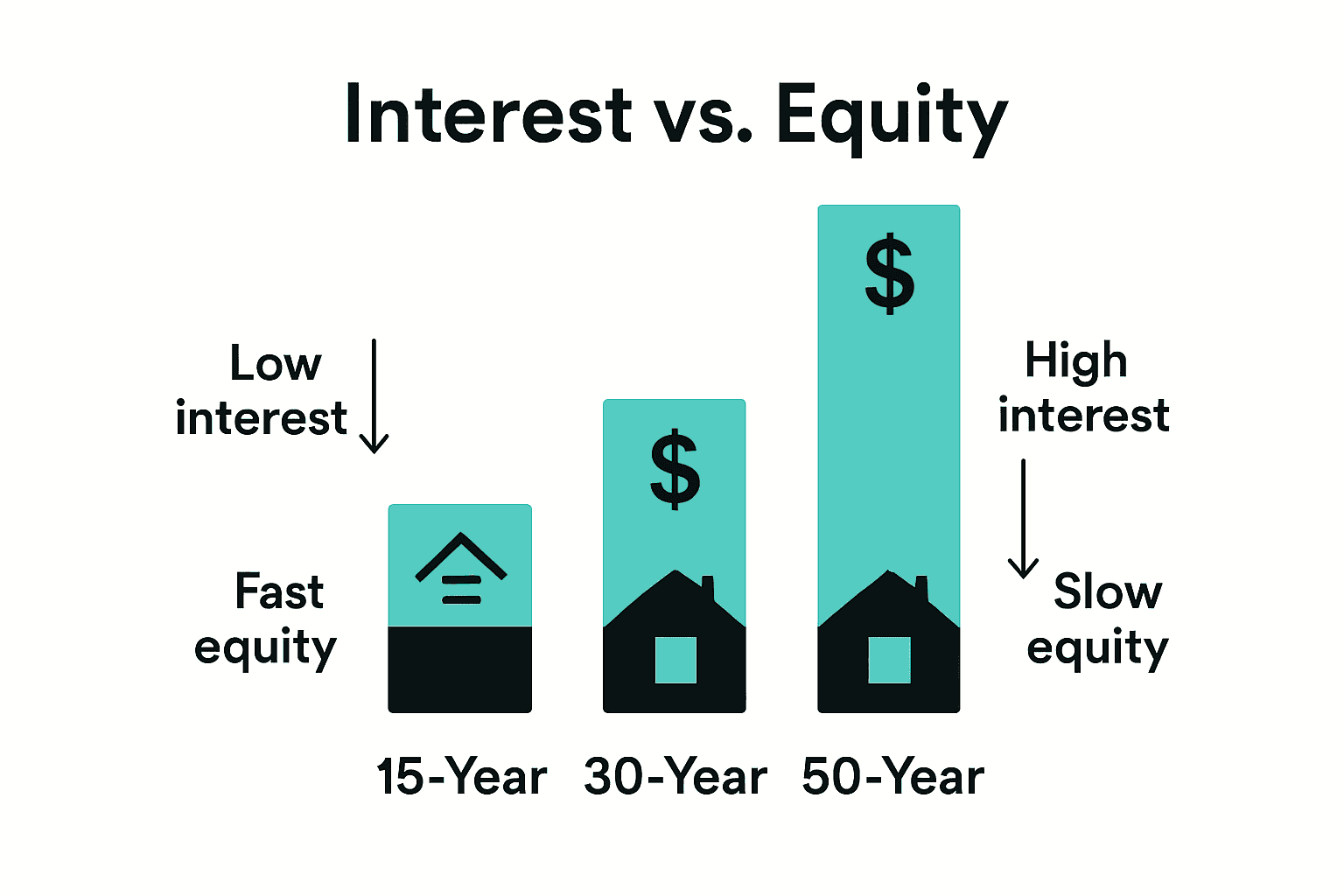

| Extended Loan Term | A 50-year mortgage allows borrowers to extend repayment over five decades, significantly reducing monthly payments. |

| Higher Total Interest | Borrowers pay substantially more in interest over the loan’s lifetime due to the extended term, which can exceed the property’s original value. |

| Slow Equity Growth | Minimal principal reduction occurs in the early years, leaving borrowers vulnerable to market fluctuations. |

| Niche Usage | Ideal for high-cost markets or buyers seeking lower immediate costs, it requires careful financial assessment and understanding of risks. |

What Is a 50‑Year Mortgage?

A 50-year mortgage represents an extended home financing option that allows borrowers to spread their loan repayment over an unprecedented five decades. Unlike traditional 15 or 30-year mortgages, this ultra-long-term loan dramatically reduces monthly payments by extending the repayment timeline to its absolute maximum. While rare in the mainstream lending market, these mortgages offer a unique strategy for buyers seeking lower immediate financial strain.

The core mechanics of a 50-year mortgage differ significantly from standard home loans. Borrowers receive an extremely extended amortization schedule where principal and interest payments are calculated across 600 months instead of the conventional 180 or 360 months. This extended timeline means dramatically lower monthly payments, but also substantially higher total interest paid over the loan’s lifetime. Typically, these loans feature adjustable interest rates, which can introduce additional financial complexity and potential risk for homeowners.

Key Characteristics of 50-Year Mortgages

- Loan term spans 50 full years

- Substantially lower monthly payment compared to shorter-term mortgages

- Often feature adjustable interest rates

- Minimal principal reduction in early repayment years

- Higher total interest costs over loan lifecycle

Financial experts generally recommend 50-year mortgages only for specific scenarios. These might include buyers in high-cost real estate markets like Hawaii, investors seeking minimal short-term cash flow obligations, or individuals anticipating significant future income increases. The extended loan term provides flexibility but comes with considerable long-term financial trade-offs that require careful personal financial analysis.

While innovative, 50-year mortgages remain a niche product not widely offered by most traditional lenders. Potential borrowers should thoroughly understand the complex financial implications, comparing total loan costs against potential benefits. Consulting with a financial advisor can help determine whether this unconventional mortgage structure aligns with individual financial goals and risk tolerance.

How 50‑Year Mortgages Work

Understanding the mechanics of a 50-year mortgage requires diving deep into its unique financial structure. Unlike traditional home loans, these extended-term mortgages fundamentally reshape how borrowers approach long-term property financing. The primary distinction lies in the extraordinary loan duration, which stretches repayment across an unprecedented half-century, dramatically altering the standard mortgage calculation methods.

The loan’s mathematical framework operates through a complex amortization schedule that prioritizes minimal monthly payments over rapid principal reduction. In the initial decades, a significant portion of each payment goes toward interest rather than building home equity. This means borrowers will experience extremely slow principal reduction in the early years of the mortgage.

For instance, during the first 10-15 years, a borrower might pay tens of thousands of dollars while barely decreasing the original loan balance.

For instance, during the first 10-15 years, a borrower might pay tens of thousands of dollars while barely decreasing the original loan balance.

Key Operational Components

- Extended Amortization: Payments spread across 600 months

- Interest-Heavy Initial Years: More money allocated to interest

- Adjustable Rate Mechanism: Typically feature variable interest rates

- Minimal Equity Building: Slow principal reduction strategy

Most 50-year mortgages incorporate adjustable-rate structures, which means the interest rate can fluctuate periodically based on market conditions. This introduces an additional layer of financial complexity and potential risk. Borrowers must carefully assess their long-term financial stability and risk tolerance, understanding that rate changes could significantly impact monthly payment amounts. The loan’s design inherently favors short-term affordability over long-term financial efficiency.

The practical application of 50-year mortgages requires sophisticated financial planning. Borrowers must recognize that while monthly payments remain lower, the total interest paid over the loan’s lifetime can be substantially higher compared to traditional 15 or 30-year mortgages. This makes these loans particularly suitable for specific scenarios such as high-cost real estate markets, investment properties, or situations where immediate cash flow flexibility takes precedence over long-term equity accumulation.

Calculated Pros for Buyers

50-year mortgages represent a strategic financing option that offers unique advantages for specific types of homebuyers. According to BadCredit, these extended-term loans make homeownership more accessible, particularly for younger buyers seeking to enter competitive real estate markets. The primary benefit lies in dramatically reduced monthly payments, which can open doors to property ownership that might otherwise seem financially impossible.

As CGAA explains, the reduced monthly financial burden allows buyers to potentially purchase larger or more desirable properties than traditional mortgage structures permit. This can be especially transformative in high-cost real estate markets like Hawaii, where property values consistently challenge typical financing models.

Buyers can strategically leverage the lower monthly payments to manage their cash flow more effectively, allocating funds toward other financial goals or investments.

Strategic Advantages for Buyers

- Enhanced Affordability: Lower monthly payments expand purchasing power

- Flexible Cash Management: Reduced mortgage costs free up monthly income

- Market Entry Opportunity: Enables younger buyers to purchase sooner

- Property Upgrade Potential: Allows consideration of more expensive properties

Beyond immediate affordability, 50-year mortgages offer nuanced financial flexibility. They can be particularly advantageous for professionals with anticipated income growth, real estate investors seeking minimal short-term obligations, or individuals in transitional career stages. The extended loan term provides a financial buffer, allowing borrowers to strategically manage their resources while securing long-term real estate assets.

However, potential buyers must approach these mortgages with comprehensive financial understanding. While the lower monthly payments are attractive, the long-term cost implications require careful consideration. Borrowers should conduct thorough personal financial analysis, potentially consulting with financial advisors to determine whether a 50-year mortgage aligns with their specific economic goals and risk tolerance.

Major Drawbacks and Financial Risks

The 50-year mortgage comes with substantial financial pitfalls that potential borrowers must carefully evaluate. According to OPB, the most significant drawback is the dramatically higher total interest payments over the loan’s lifetime, which can substantially exceed the property’s original purchase price. This extended repayment structure means borrowers will pay exponentially more in interest compared to traditional 15 or 30-year mortgage terms.

Mises highlights another critical risk: minimal equity buildup during the initial years of the mortgage. This slow principal reduction leaves borrowers extremely vulnerable, particularly in scenarios of property value fluctuations. The prolonged timeline means that for decades, a significant portion of monthly payments will be absorbed by interest rather than building meaningful home equity.

Critical Financial Vulnerabilities

- Massive Interest Accumulation: Total interest paid can exceed original property value

- Extremely Slow Equity Growth: Minimal principal reduction in early decades

- Market Volatility Exposure: High risk during property value downturns

- Long-Term Financial Inflexibility: Restricted refinancing or selling options

The financial complexity of 50-year mortgages extends beyond immediate monetary considerations. Borrowers face potential long-term constraints that could significantly impact their financial mobility. The extended loan term may not align with typical career trajectories, retirement planning, or life stage transitions.

This misalignment can create substantial financial stress, especially if income expectations or personal circumstances change dramatically over the loan’s extended duration.

This misalignment can create substantial financial stress, especially if income expectations or personal circumstances change dramatically over the loan’s extended duration.

Ultimately, 50-year mortgages represent a high-risk financial strategy that demands extraordinary financial discipline and foresight. Potential borrowers must conduct comprehensive financial modeling, considering worst-case scenarios and understanding the profound long-term implications. Professional financial consultation becomes crucial in determining whether these unconventional mortgage structures genuinely serve an individual’s economic objectives or potentially compromise their financial future.

Alternatives to 50‑Year Mortgages

Homebuyers seeking financial flexibility have several mortgage alternatives that offer more balanced approaches to property financing. Traditional 30-year fixed-rate mortgages remain the most popular option, providing a predictable payment structure with reasonable monthly obligations and faster equity accumulation. These conventional loans strike a critical balance between affordability and long-term financial health, making them an attractive alternative for most buyers.

Another compelling alternative is the 15-year fixed-rate mortgage, which accelerates equity building and significantly reduces total interest paid over the loan’s lifetime. While monthly payments are higher compared to 30-year or 50-year options, borrowers can save substantial money and own their property outright much faster. This approach particularly appeals to buyers with stable, higher incomes who can manage increased monthly financial commitments.

Strategic Mortgage Alternatives

- 30-Year Fixed-Rate Mortgage: Standard market option with balanced terms

- 15-Year Fixed-Rate Mortgage: Faster equity accumulation

- Adjustable-Rate Mortgages (ARMs): Lower initial interest rates

- Hybrid Loan Structures: Combinations of fixed and adjustable rates

Additional innovative financing strategies include hybrid loan structures that combine elements of fixed and adjustable-rate mortgages. These options can provide initial lower payments with potential rate adjustments, offering more flexibility than traditional long-term mortgages. Government-backed loan programs like FHA, VA, and USDA loans also present unique alternatives, especially for first-time homebuyers or those with specific financial circumstances.

Potential borrowers should carefully evaluate their personal financial situation, long-term goals, and risk tolerance when selecting a mortgage alternative. Consulting with financial advisors or mortgage professionals can help identify the most suitable financing strategy, considering factors like income stability, future earning potential, and overall economic objectives. The right mortgage isn’t just about monthly affordability—it’s about creating a sustainable path to homeownership that aligns with individual financial health and lifestyle aspirations.

Make Smart Financing Decisions for Your Oahu Condo Purchase

Navigating the complexities of a 50-year mortgage requires careful thought about long-term costs and financial risks. If you are considering this loan option to lower your monthly payment and gain flexibility, it is equally important to explore the right condo opportunities that align with your financial goals here on Oahu. Understanding terms like adjustable rates and slow equity buildup can help you plan effectively before committing to a property investment or lifestyle purchase.

Start your property search with confidence at BuyOahuCondos.com, where you can explore detailed neighborhood guides, compare condos, and get insights into HOA fees and rental policies. Take control of your home buying journey by requesting customized property lists or scheduling personalized tours today. Don’t wait to turn your homeownership aspirations into reality with trusted resources tailored to your unique financial situation.

Frequently Asked Questions

What is a 50-year mortgage?

A 50-year mortgage is a long-term home financing option that allows borrowers to spread their repayments over 50 years, resulting in lower monthly payments compared to traditional 15 or 30-year mortgages.

What are the main advantages of a 50-year mortgage?

The main advantages include lower monthly payments, enhanced affordability, and greater flexibility for cash management, allowing buyers to enter high-cost real estate markets. It can also be beneficial for individuals expecting significant future income increases.

What are the disadvantages of a 50-year mortgage?

A 50-year mortgage can result in significantly higher total interest payments over its lifetime and very slow equity growth during the early years. It also exposes borrowers to increased financial risk if property values fluctuate.

How do 50-year mortgages work compared to traditional mortgages?

50-year mortgages have an extended amortization schedule of 600 months, resulting in lower monthly payments but also higher total interest paid compared to standard 15 or 30-year mortgages, which generally focus more on principal reduction in the early years.