Oahu Condo Financing Explained: Complete Guide

Our oahu condo financing explained, Did you know that over 40 percent of home purchases in Oahu involve condos rather than single-family homes? Financing a condo here can be far more complex than it looks, with unique local lender rules, association requirements, and strict building qualifications affecting your options. Knowing how these factors work together helps buyers avoid costly mistakes and opens up a wider range of possibilities in Hawaii’s competitive property market.

oahu condo financing explained Table of Contents

- Understanding Oahu Condo Financing Basics

- Types of Loans for Oahu Condos

- Eligibility Requirements and Down Payment Rules

- How HOA Fees Impact Financing Approval

- Financing Mistakes to Avoid in Hawaii

Key Takeaways

| Point | Details |

|---|---|

| Understanding Unique Financing | Oahu condo financing requires knowledge of local lender requirements and association regulations distinct from mainland markets. |

| Loan Program Options | Buyers can choose from several financing routes, including FHA, VA, USDA, and AHO programs, each with specific eligibility and benefits. |

| Importance of HOA Fees | HOA fees significantly impact financing approval; lenders assess financial health of associations as part of the mortgage approval process. |

| Avoiding Common Mistakes | Prospective buyers should conduct thorough research on condo associations and financing criteria to prevent costly errors and ensure financing success. |

Understanding Oahu Condo Financing Basics

Navigating the complex landscape of condo financing in Oahu requires understanding several unique local considerations. Mortgage options for condominiums differ significantly from traditional single-family home financing, presenting both opportunities and challenges for potential buyers. Unlike mainland markets, Oahu’s real estate environment demands specialized knowledge about lender requirements, association regulations, and financial prerequisites.

According to the Honolulu Condo Investment Guides, key financing factors include loan type, down payment, and building approval status. Lenders typically examine condo association health, reserve funds, owner-occupancy ratios, and insurance coverage before approving financing. This means buyers must not only qualify personally but also ensure the specific condo development meets strict institutional lending standards.

Special programs can provide strategic advantages for certain buyers. The Office of Hawaiian Affairs offers the AHO program, specifically designed to reduce homeownership barriers for Native Hawaiians by facilitating lower down payments and eliminating private mortgage insurance. Meanwhile, Federal Housing Administration (FHA) loans provide alternative financing paths with more flexible credit requirements, though they come with their own set of complex eligibility criteria.

Prospective buyers should prepare comprehensive financial documentation, including credit reports, income verification, and detailed asset statements. Understanding these nuanced financing dynamics will empower you to navigate Oahu’s unique real estate market more effectively and increase your chances of securing the right condo financing strategy.

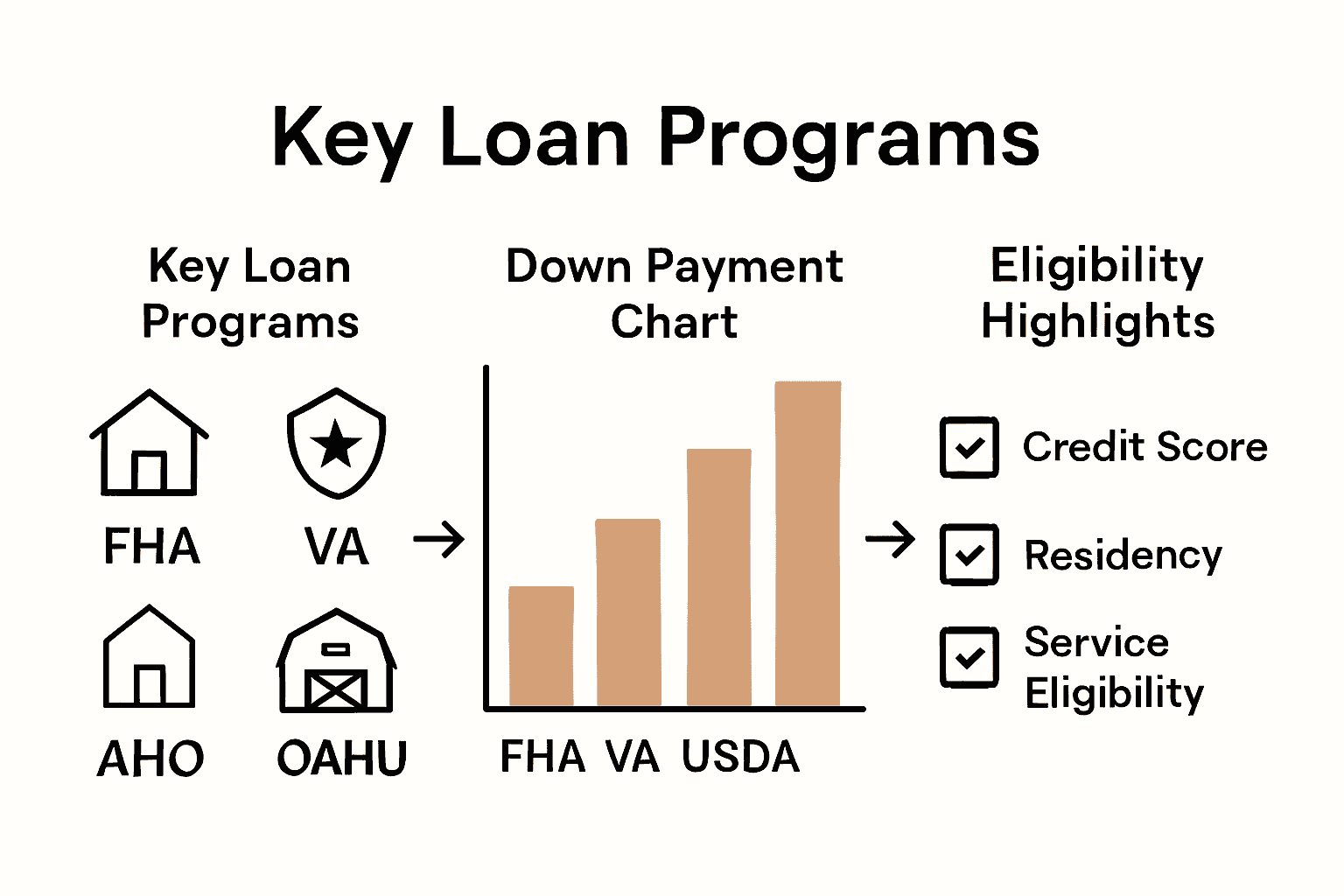

Types of Loans for Oahu Condos

Oahu condo buyers have multiple financing pathways designed to accommodate diverse financial situations and homeownership goals. Understanding the nuanced loan options can significantly impact your purchasing strategy and overall affordability in Hawaii’s competitive real estate market.

According to HUD research, Federal Housing Administration (FHA) loans provide an attractive entry point for many buyers. These loans require as little as 3.5% down payment and offer more flexible credit requirements, making them particularly appealing for first-time homebuyers or those with moderate credit profiles. Oahu Condo Buying Tips highlight that FHA loans can be especially beneficial for condominiums, provided the specific development meets certain approval standards.

Veterans and active military personnel have exceptional opportunities through VA loans, which offer zero down payment options and typically feature more competitive interest rates. For those in rural or suburban areas surrounding Oahu, USDA loans present another zero down payment alternative with potentially lower mortgage insurance costs. These specialized loan programs reflect the diverse financing landscape available to Hawaii’s condo buyers.

Navigating these loan types requires careful consideration of personal financial health, long-term housing goals, and specific condo development requirements.

Each loan program comes with unique qualification criteria, down payment expectations, and potential restrictions. Prospective buyers should consult with local mortgage professionals who understand Oahu’s distinctive real estate market to determine the most suitable financing approach for their individual circumstances.

Each loan program comes with unique qualification criteria, down payment expectations, and potential restrictions. Prospective buyers should consult with local mortgage professionals who understand Oahu’s distinctive real estate market to determine the most suitable financing approach for their individual circumstances.

Here’s a comparison of major condo loan programs available in Oahu:

| Loan Program | Down Payment | Key Eligibility | Unique Benefits |

|---|---|---|---|

| FHA Loan | 3.5% minimum | 580+ credit score Condo must be FHA approved | Flexible credit Low down payment |

| VA Loan | 0% | Veteran/active duty VA eligibility | No PMI Competitive rates |

| USDA Loan | 0% | Eligible rural area Income limits | No PMI Low upfront fees |

| AHO Program | 3% | Native Hawaiian Local resident | No PMI Lower entry costs |

Eligibility Requirements and Down Payment Rules

Condo financing in Oahu involves intricate eligibility criteria and down payment structures that vary significantly across different loan programs. Potential buyers must navigate a complex landscape of requirements that extend beyond traditional home financing, making thorough preparation essential for successful condo purchases.

According to the Office of Hawaiian Affairs, the AHO program offers a unique opportunity for Native Hawaiian first-time homebuyers. This specialized initiative requires applicants to be Native Hawaiian, current Hawaii residents, and provides a reduced down payment of just 3%, while eliminating private mortgage insurance. Affordable Condos Honolulu emphasizes that such targeted programs can dramatically lower initial financial barriers for qualified individuals.

Federal loan programs present diverse eligibility pathways with distinct requirements. FHA loans accommodate borrowers with credit scores of 580 or higher, demanding a minimal 3.5% down payment. Veterans enjoy even more advantageous terms through VA loans, which offer zero down payment for eligible service members. Similarly, USDA loans provide no down payment options for properties in designated rural areas surrounding Oahu, expanding financing possibilities for different buyer profiles.

Prospective condo buyers should meticulously assess their personal financial situation, credit history, and specific loan program requirements. Each financing option comes with unique qualification standards, including income limits, debt-to-income ratios, and property type restrictions. Consulting with local mortgage professionals who specialize in Oahu’s real estate market can help buyers identify the most suitable financing strategy tailored to their individual circumstances.

How HOA Fees Impact Financing Approval

Homeowners Association (HOA) fees play a critical role in determining the financial viability of condo financing in Oahu, creating a complex landscape that potential buyers must carefully navigate. These recurring expenses are more than just monthly charges; they directly influence lenders’ decisions about mortgage approvals and overall property investment potential.

According to HUD guidelines, lenders meticulously examine HOA financial health as a key criterion for financing approval. This involves comprehensive analysis of reserve funds, maintenance budgets, and overall association financial management. Honolulu Condos for Sale highlights that lenders typically require condominiums to demonstrate robust financial stability, with specific attention to owner-occupancy rates and adequate reserve funds to cover potential maintenance and repair expenses.

The impact of HOA fees extends beyond monthly budgeting. FHA loans, in particular, impose strict requirements on condominium associations, mandating that they maintain adequate reserve funds typically ranging between 10% to 20% of their annual budget. These financial criteria can significantly affect a buyer’s ability to secure financing, as lenders view the association’s fiscal management as a direct reflection of the property’s long-term value and investment potential.

Prospective condo buyers should conduct thorough due diligence, carefully reviewing HOA financial statements, understanding fee structures, and assessing the potential for future fee increases. Factors such as special assessments, maintenance history, and the association’s approach to financial planning can dramatically influence both financing approval and the overall cost of ownership. Consulting with local real estate professionals who understand Oahu’s unique condo market can provide invaluable insights into navigating these complex financial considerations.

Financing Mistakes to Avoid in Hawaii

Navigating the complex condo financing landscape in Hawaii requires strategic awareness and proactive planning. Financing pitfalls can derail even the most well-intentioned real estate investments, making it crucial for buyers to understand the unique challenges of Oahu’s property market.

According to HUD guidelines, one of the most significant mistakes first-time buyers make is overlooking condominium-specific approval criteria. Is Buying a Condo in Honolulu a Smart Investment warns that many condominiums fail to meet critical FHA requirements, particularly regarding owner-occupancy rates. These restrictions can unexpectedly limit financing options, potentially forcing buyers to seek alternative mortgage strategies or choose different properties.

Financial preparedness goes beyond credit scores and down payments. Prospective buyers often underestimate the importance of comprehensive financial documentation and thorough condo association research. Common mistakes include neglecting to review HOA financial statements, failing to understand special assessment potentials, and not budgeting for potential fee increases. These oversights can create significant long-term financial strain and complicate mortgage approval processes.

To mitigate risks, potential buyers should consult HUD-approved housing counselors who specialize in Hawaii’s unique real estate market. Developing a comprehensive understanding of local financing nuances, maintaining flexible expectations, and conducting meticulous due diligence can help buyers avoid costly mistakes and successfully navigate Oahu’s intricate condo financing landscape.

Take Control of Your Oahu Condo Financing Journey Today

Understanding the complexities of condo financing in Oahu can feel overwhelming, especially when facing strict loan eligibility rules, HOA fee implications, and specialized programs like FHA or AHO. If you want to avoid common pitfalls and feel confident navigating lender requirements and association standards, you need clear guidance and up-to-date resources tailored to Hawaii’s unique market.

Discover the most effective strategies with expert insights on Oahu Condo Buying Tips | Honolulu & Waikiki Advice and deepen your knowledge with comprehensive Honolulu Condo Investment Guides | ROI & Rental Tips. Don’t wait to secure your future condo with the right financing approach. Visit BuyOahuCondos.com now to explore listings, assess your options, and request personalized support that turns complicated financing into manageable steps.

Frequently Asked Questions

What types of loans are available for financing a condo in Oahu?

Oahu condo buyers can choose from several loan options, including Federal Housing Administration (FHA) loans, VA loans for veterans and active military, USDA loans for rural properties, and the AHO program for Native Hawaiian residents. Each option has specific down payment requirements and eligibility criteria.

How do HOA fees affect financing approval for condos?

HOA fees are crucial in financing approvals as lenders evaluate the financial health of the homeowners association. This includes reviewing reserve funds and owner-occupancy rates. Strong HOA financial management can enhance a buyer’s chances of obtaining financing, while poor management may hinder approval.

What are the eligibility requirements for FHA loans in Oahu?

To qualify for FHA loans in Oahu, borrowers generally need a credit score of 580 or higher and a minimum down payment of 3.5%. Additionally, the condo must meet specific FHA approval standards, which includes having a healthy condo association.

What financing mistakes should buyers avoid when purchasing a condo?

Common mistakes include neglecting to review the condo association’s financial statements, underestimating the impact of HOA fees, and overlooking condominium-specific approval criteria. Thorough due diligence and consulting local mortgage professionals can help mitigate these risks.

13 Comments